What Are the Top Investing Mistakes Made by Tech Pros?

Learn the top investing mistakes tech professionals make, from overconcentration to poor tax planning, and how to avoid them with smart strategies.

Tech professionals are often highly compensated, especially through equity-based compensation. But with higher income and complex benefits come greater risks, particularly when it comes to investing. Here are some of the most common investing mistakes I see among tech professionals:

1. Overconcentration

Tech professionals who receive equity compensation like RSUs, ESPPs, and ISOs, may quickly accumulate significant positions in company stock, leading to lopsided investment portfolios. Owning too much of your company stock creates what is known as concentration risk. This might result in “airplane money” (a sudden windfall), but it could just as easily lead to significant losses.

It is also common for tech people to invest in what they know, which is usually more technology. When I review investment statements of prospective clients, I often see portfolios loaded with different tech stocks. But make no mistake: that's not diversification. That's just tech sector risk. Most of us remember what happened in 1999-2000.

Broad diversification among several thousands of stocks helps to create guardrails. And yes, it will limit your upside potential, relative to the single stock or sector positions. True diversification can improve the reliability and consistency of your investment outcomes by reducing risk and uncertainty.

2. Overconfidence

Too many people foolishly attempt to time the markets or specific stocks. They may believe that they can predict the future based on past performance, or they might be emotionally reacting to the markets in the moment. Either way, overconfidence can be problematic when it comes to investing.

We believe markets are efficient, meaning prices already reflect the collective wisdom of all participants. There is little compelling evidence that anyone can reliably and consistently predict the markets with success.

Trying to outguess the market is like trying to beat a supercomputer at chess with your eyes closed. Instead, embrace an evidence-based strategy. Let markets work for you, rather than trying to outsmart them!

3. No Tax-Smart Asset Placement

Too often, I see high earners holding tax-inefficient investments in taxable accounts, while also holding tax-efficient assets in tax-deferred accounts.

For example, one tech pro had a large bond position sitting in a taxable brokerage account. The problem? Bond interest is taxed as ordinary income, and this person was in the 37% tax bracket. Ouch! A mistake like this can have steep tax consequences, but it is avoidable with tax-smart asset placement.

Different account types have different tax characteristics:

- Traditional IRA: Tax-deferred growth until withdrawal

- Roth IRA: Tax-free growth and tax-free qualified withdrawals.

- Taxable account: No shelter. Interest, dividends, and capital gains are taxed at varied rates

By strategically placing the right investments in the right accounts, you can reduce taxes and improve after-tax returns. We help clients do just that.

4. Home Bias

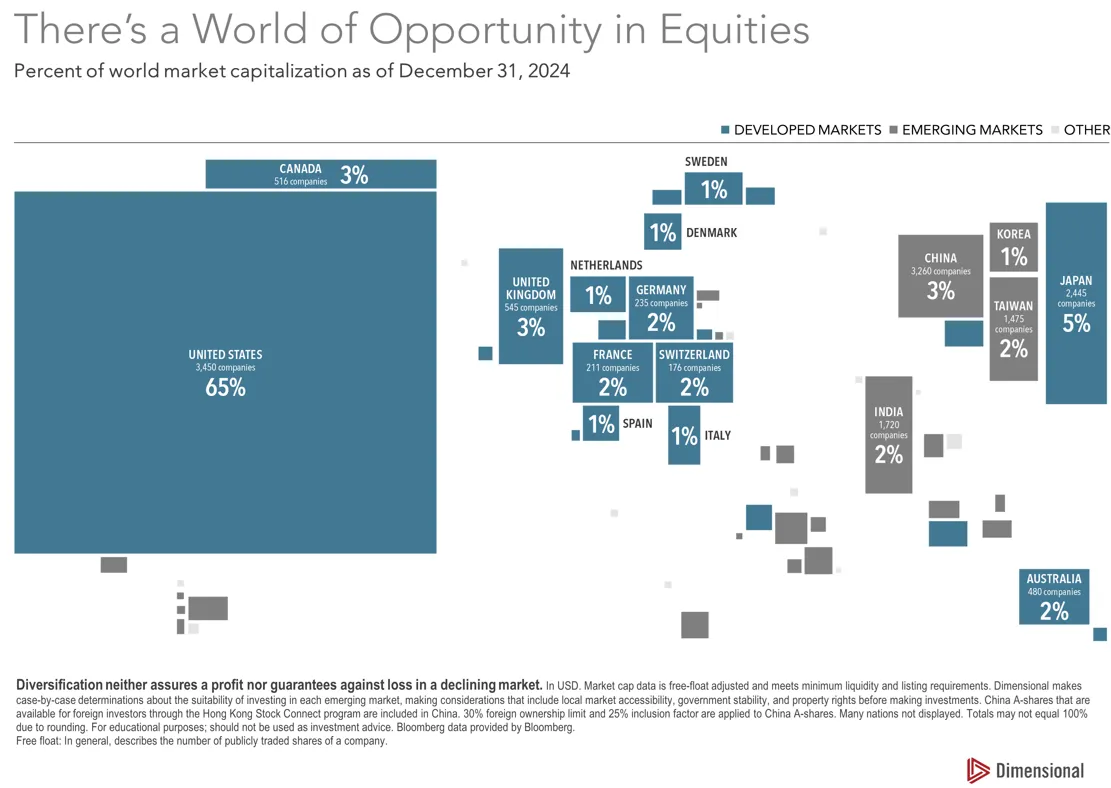

Did you know the United States makes up about 65% of global market capitalization? And yet, most investors I meet hold 80-100% of their stocks in U.S. companies.

Imagine shopping in only 1 or 2 of the 10 available aisles at your local grocery store. That sounds odd, right? Why limit yourself to only a few aisles? But that is what you are doing when you stick mainly to the U.S.

When you look at your own investment portfolio, what percentage is held in U.S. positions?

Home bias is the tendency of investors to allocate a sizable portion of their investments to domestic assets. The result is a lack of international exposure. And this is not just unique to Americans. In 2023, Vanguard noted1 that Canadians held around 50% of their equity in Canadian companies, even though Canada only accounts for 2% of the global market.

As of December 20242, there were over 20,000 global stocks:

- 3,450 in the U.S.

- 6,274 in developed markets outside the U.S.

- 10,390 in emerging markets

If you are only investing in U.S. stocks, you are ignoring 16,600+ global opportunities.

The point is that international markets, both developed and emerging markets, offer investors the opportunity to further diversify and improve their investment outcomes. But beware of the potential volatility often associated with international investing.

Another issue with home bias is that you are over-relying on one country to drive your investment experience. Recall earlier that we discussed overconcentration risk. Home bias is the overconcentration of one country in your investment portfolio.

Here is a fun fact: Over the last 20 years, the U.S. was the best performing developed market only once, in 2014.

But perhaps most striking is the historical spread between the best and worst performing countries in any given year. The spread in 2009 was nearly 81%. This data suggests the importance of diversifying globally, and not just investing in the U.S.

If you are only investing in U.S. positions, then you are potentially missing the opportunity to expand your eligible investment universe, and you may be overconcentrating your equity risk.

5. Lack of Small and Mid-Cap Exposure

Many investors think they are diversified because they own the S&P 500. But that is just large cap U.S. stocks. What about the other 3,000+ U.S. companies?

What percentage of your domestic equity is allocated to small and mid-cap stocks?

Small and mid-cap stocks offer more room for growth and broader diversification. But they are often left out of investment portfolios altogether. While they can be more volatile, they also provide unique return potential over time.

6. No Investment Policy Statement

Let’s be honest. Many tech professionals are winging it with their investments. It is common.

When I review portfolios, there is usually no clear strategy or process for these areas:

- Investment philosophy

- Asset allocation

- Security selection and monitoring

- Aligning investments with risk tolerance

- Tax-smart asset placement

- Rebalancing and tax harvesting

An Investment Policy Statement (IPS) lays the groundwork for all investment decisions. It defines:

- Your investment goals and time horizon

- Your asset allocation

- Risk tolerance

- Guidelines for rebalancing, tax harvesting, and more

An IPS is like a product roadmap. It helps you stay aligned with long-term objectives and resist the urge to pivot every time the market throws a bug your way.

Do you have an Investment Policy Statement? Or are you winging it?

Final Thoughts

Tech professionals have access to tremendous financial tools. But even smart people can make costly investing mistakes. The good news? These mistakes are avoidable with the right strategy, discipline, and structure.

At TwoTen Planning, I help tech professionals in Austin and beyond align their investments with their goals, reduce unnecessary risk, and invest with confidence.

If you’re ready to clean up your investment strategy, let’s talk.

Citations

Dimensional. (2024). Pursuing A Better Investment Experience. Austin, TX.

Aspects of our investment philosophy reflect the opinions of TwoTen Planning, PLLC.

1Sources: IMF’s Coordinated Portfolio Investment Survey 2023. Market cap data and holdings as of 4/30/2024.

2Disclosure for the number of 2024 stocks:

The foregoing content reflects the opinions of TwoTenPlanning and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as financial, legal, tax, or investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. All investing involves risk, including the potential for loss of principal. There is no guarantee or assurance that diversification, strategies based on Nobel prize-winning research, or any investment plan or strategy will be successful. Past performance may not be indicative of future results. Discuss your specific tax issues with a qualified tax professional.

More Free Resources?

Sign up and receive our complimentary guide plus FREE regular updates!

Our Most Recent Blogs

Check out our most recent blogs where we share insightful articles, trends, and news from a Christ-centred perspective in the financial industry.

“For we are His workmanship, created in Christ Jesus for good works, which God prepared beforehand that we should walk in them.”